Within Saving

When saving first does more harm

Saving before spending fails when the transfer is too high, emergency access is too difficult, or debt becomes more expensive.

On this page

- The danger of saving while borrowing expensively

- Signs the default amount is unrealistic

- How to review the system without abandoning it

Page outline Jump by section

Introduction

Saving before spending is one of the most effective personal-finance habits because it turns saving into the default. However, a useful self-improvement practice is not the same as an unbreakable rule. A saving system can backfire when it leaves someone short of cash for ordinary expenses, forces them to borrow at high interest rates, or locks money away so effectively that they cannot use it when they genuinely need it.

The goal of saving first is greater resilience, not the appearance of discipline. If a transfer to savings repeatedly causes overdrafts, credit-card balances, missed bills or financial stress, the system is working against its purpose. Research consistently shows that emergency savings improve financial security and reduce hardship, but those benefits depend on saving in a way that strengthens day-to-day stability rather than undermining it. Financial Health Network[Consumer Financial Protection Bureau]files.consumerfinance.govSource details in endnotes.

The goal of saving first is greater resilience, not the appearance of discipline. If a transfer to savings repeatedly causes overdrafts, credit-card balances, missed bills or financial stress, the system is working against its purpose. Research consistently shows that emergency savings improve financial security and reduce hardship, but those benefits depend on saving in a way that strengthens day-to-day stability rather than undermining it. Financial Health Network[Consumer Financial Protection Bureau]files.consumerfinance.govSource details in endnotes.

The danger of saving while borrowing expensively

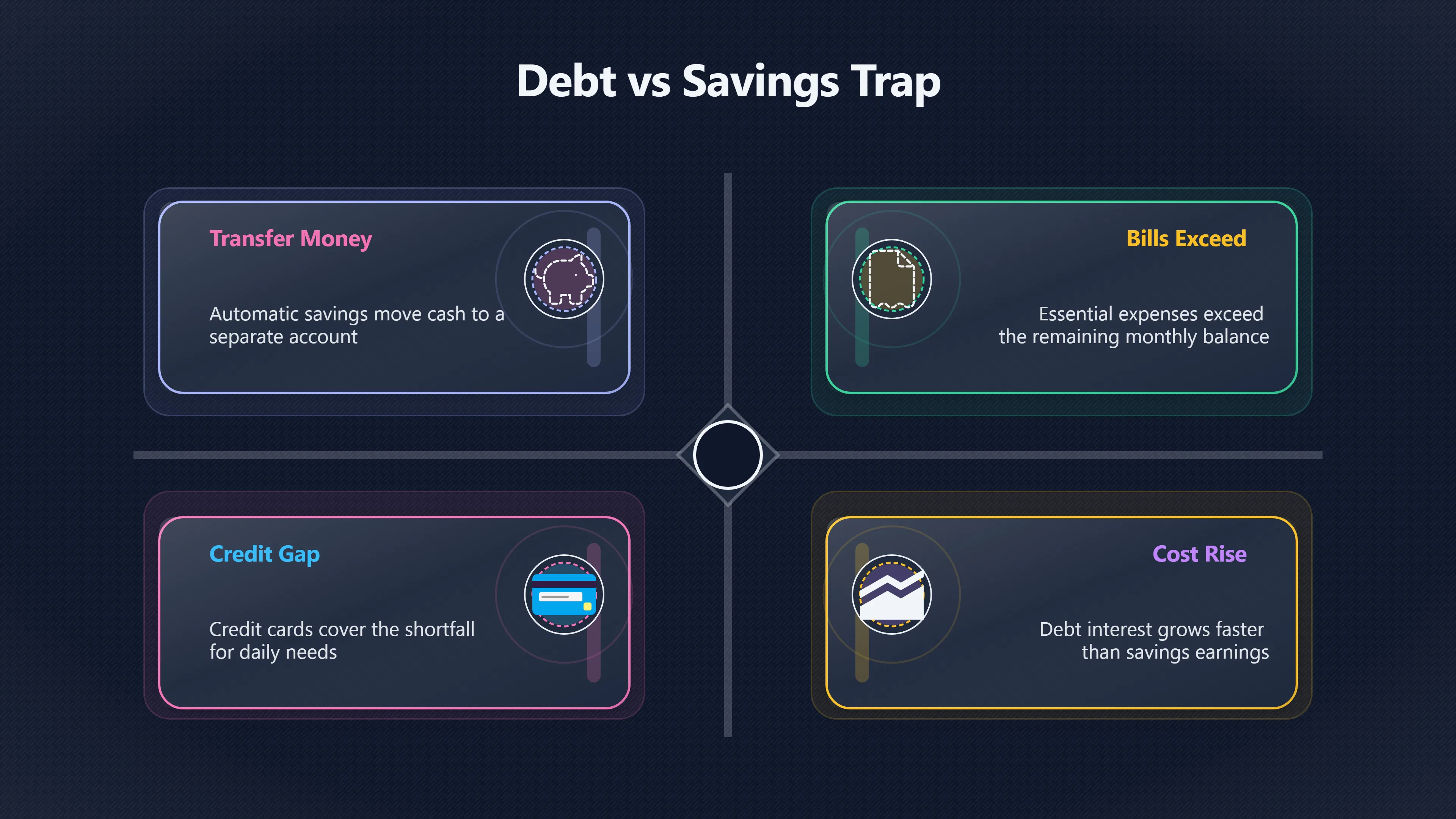

One of the clearest ways a saving-first strategy can fail is when savings grow at the same time that expensive debt grows faster.

Consider a person who automatically transfers money into a savings account every payday while carrying a credit-card balance with a much higher interest rate. The savings account may earn some interest, but the debt can accumulate interest and fees at a much faster pace. In practical terms, the household is moving money into one pocket while losing more from another.

This does not mean everyone should empty savings to eliminate debt. Emergency reserves still have value because unexpected expenses happen. The problem arises when saving targets become so aggressive that routine expenses end up being financed with credit. In that situation, the saving habit is no longer increasing resilience; it is merely shifting costs into a more expensive form. Financial guidance commonly treats interest rates, debt costs and emergency-fund needs as factors that must be balanced together rather than pursued in isolation.[Mutual of Omaha]mutualofomaha.compaying off debt vs saving what to chooseMutual of OmahaPaying Off Debt vs Saving: What to ChooseApr 27, 2026 — Primary factors to weigh when choosing between paying off debt and…[discover]discover.comsuccessfully payoff debt build emergency fundPay Off Debt or Save for an Emergency Fund?Feb 17, 2026 — Depending on your personal situation and financial goals, you may not need to c… A common warning sign is a monthly pattern like this:

- Money is transferred automatically into savings.

- Bills or essentials exceed the remaining balance.

- Credit cards or overdrafts cover the gap.

- Interest and fees accumulate.[files.consumerfinance.gov]files.consumerfinance.govConsumer Financial Protection Bureau Debt getting in your way?Get a handle on it.Con: If the interest and fees are high on your larger debts, you might pay more overall if you pay off the smaller one…

- Savings rise slowly while debt costs rise quickly.

When that cycle appears, the saving amount is probably too high for current circumstances.

When emergency access becomes too difficult

Another failure mode occurs when money is technically saved but practically unavailable.

Emergency funds exist to absorb shocks such as car repairs, temporary income loss, urgent travel or unexpected household costs. Financial guidance generally recommends keeping emergency savings accessible rather than tying all reserves up in places that are difficult, slow or costly to access.[MaPS]moneyhelper.org.ukMaPSEmergency savings – how much is enough?A good rule of thumb to give yourself a solid financial cushion is to have three to six months…[Consumer Financial Protection Bureau]files.consumerfinance.govSource details in endnotes.

People sometimes create so much friction around savings that they cannot use the money when they genuinely need it. Examples include:

- Keeping all emergency savings in accounts with withdrawal restrictions.

- Treating any withdrawal as a personal failure.

- Using savings products that create delays during urgent situations.

- Refusing to use emergency funds even when the alternative is expensive borrowing.

This can create a paradox. Someone may have cash reserves on paper but still rely on credit because accessing their own money feels difficult, complicated or psychologically forbidden.

The purpose of an emergency fund is not merely to exist. It is to be available when a genuine emergency occurs.

Signs the default amount is unrealistic

Automatic saving works because it removes repeated decision-making. Yet automation can hide problems when circumstances change.

A transfer amount that worked six months ago may no longer fit after rent increases, childcare costs, reduced hours, higher energy bills or other life changes. Because the transfer happens automatically, people sometimes interpret the resulting strain as a personal discipline problem rather than a system-design problem.

Several indicators suggest the default amount has become unrealistic:

- The current account regularly approaches zero before payday.

- Credit-card balances increase despite efforts to save.

- Bills are delayed to protect the savings transfer.

- Small emergencies repeatedly require borrowing.

- Savings contributions are frequently reversed later in the month.

- The saver feels constant financial pressure despite consistent saving.

A saving rule should make everyday finances calmer and more predictable. If it consistently creates instability, the amount rather than the principle may be wrong.

An overlooked issue is irregular spending. Annual insurance premiums, vehicle maintenance, holiday travel and home repairs are not emergencies, yet many budgets ignore them. A person may appear to be saving successfully while actually underestimating future obligations. When those predictable costs arrive, credit often fills the gap.

The hidden cost of oversaving

The phrase “pay yourself first” can sometimes be interpreted too literally. Saving more is not automatically better.

Research and financial guidance strongly support building emergency reserves because savings improve financial resilience and reduce the likelihood of hardship during shocks. Financial Health Network[Vanguard However]corporate.vanguard.comemergency savings may hold key financial well beingsavings may hold key to financial well-being29 Apr 2025 — “People with emergency savings have a higher level of financial well-being, spe…, beyond the amount needed for stability, there are trade-offs. Excess cash held purely out of habit may prevent progress on other important goals:

- Paying down expensive debt.[discover.com]discover.comsuccessfully payoff debt build emergency fundPay Off Debt or Save for an Emergency Fund?Feb 17, 2026 — Depending on your personal situation and financial goals, you may not need to c…

- Building pension or retirement savings.

- Investing for long-term growth.

- Funding education or career development.

- Maintaining necessary insurance coverage.

The problem is not saving itself. The problem is treating one financial rule as more important than the broader objective of improving overall financial health.

How to review the system without abandoning it

When saving first starts causing problems, the answer is rarely to stop saving altogether. A better response is usually to redesign the system.

Reduce the transfer before removing it

A smaller automatic transfer often preserves the behavioural advantage while relieving cash-flow pressure.

For example, reducing a transfer from 15% of income to 5% may be more effective than cancelling it entirely. The habit survives while day-to-day finances regain breathing room.

Check whether debt costs exceed the benefit

If high-interest borrowing is growing, examine whether part of the saving contribution should be redirected toward debt reduction. The objective is to avoid situations where savings rise slowly while interest charges rise faster.[Consumer Financial Protection Bureau]files.consumerfinance.govSource details in endnotes.

Separate true emergencies from predictable expenses

Many financial crises are actually foreseeable costs. Creating dedicated pots for annual bills, vehicle maintenance or household repairs can reduce the need to raid emergency savings or use credit later.

Reassess after major life changes

Income changes, housing costs, family circumstances and inflation can all alter what is sustainable. A saving percentage that once felt effortless may become unrealistic, while a percentage that was once difficult may become too conservative after a pay rise.

A good saving system should reduce stress

The strongest version of saving before spending is flexible rather than rigid. It protects against financial shocks, reduces dependence on debt and creates long-term security. When it starts producing overdrafts, expensive borrowing or chronic cash shortages, the issue is usually not the idea of saving first but the way the rule has been implemented.

A successful saving habit should leave someone more resilient after ordinary bills are paid. If it repeatedly pushes routine expenses onto costly credit, the system is no longer serving its purpose and deserves adjustment. The best saving rule is not the most aggressive one. It is the one that consistently improves financial stability over time.

Amazon book picks

Further Reading

Books and field guides related to When saving first does more harm. Use these as the next step if you want deeper reading beyond the article.

I Will Teach You to Be Rich

Addresses cash flow, debt and realistic automation levels.

Your Money or Your Life

Encourages sustainable saving rather than self-defeating austerity.

The Total Money Makeover

Rating: 4.5/5 from 16 Google Books ratings

Discusses trade-offs between debt reduction and saving.

eBay marketplace picks

Marketplace Samples

Example marketplace items related to this page. Use the search link to explore similar finds on eBay.

Endnotes

1.

Source: discover.com

Title: successfully payoff debt build emergency fund

Link:https://www.discover.com/personal-loans/resources/consolidate-debt/successfully-payoff-debt-build-emergency-fund/

Source snippet

Pay Off Debt or Save for an Emergency Fund?Feb 17, 2026 — Depending on your personal situation and financial goals, you may not need to c...

2.

Source: corporate.vanguard.com

Title: emergency savings may hold key financial well being

Link:https://corporate.vanguard.com/content/corporatesite/us/en/corp/articles/emergency-savings-may-hold-key-financial-well-being.html

Source snippet

savings may hold key to financial well-being29 Apr 2025 — “People with emergency savings have a higher level of financial well-being, spe...

3.

Source: debt.org

Title: should i empty my savings to pay off credit card

Link:https://www.debt.org/credit/cards/should-i-empty-my-savings-to-pay-off-credit-card/

Source snippet

Should I Empty My Savings To Pay off My Credit Card?Sep 6, 2024 — We'll help you navigate the tough decision of whether to use your savin...

4.

Source: files.consumerfinance.gov

Link:https://files.consumerfinance.gov/f/documents/cfpb_mem_emergency-savings-financial-security_report_2022-3.pdf

5.

Source: consumerfinance.gov

Title: an essential guide to building an emergency fund

Link:https://www.consumerfinance.gov/an-essential-guide-to-building-an-emergency-fund/

Source snippet

Consumer Financial Protection BureauAn essential guide to building an emergency fund29 Oct 2025 — An emergency fund is a cash reserve tha...

6.

Source: mutualofomaha.com

Title: paying off debt vs saving what to choose

Link:https://www.mutualofomaha.com/advice/financial-planning/managing-debt/paying-off-debt-vs-saving-what-to-choose

Source snippet

Mutual of OmahaPaying Off Debt vs Saving: What to ChooseApr 27, 2026 — Primary factors to weigh when choosing between paying off debt and...

7.

Source: consumerfinance.gov

Link:https://www.consumerfinance.gov/about-us/blog/servicemembers-immediate-actions-financial-success-pay-down-debt-make-plan-start-early/

Source snippet

Consumer Financial Protection Bureaupay down debt, make a plan, start earlyOct 1, 2018 — The immediate actions toward financial freedom i...

8.

Source: moneyhelper.org.uk

Link:https://www.moneyhelper.org.uk/en/savings/types-of-savings/emergency-savings-how-much-is-enough

Source snippet

MaPSEmergency savings – how much is enough?A good rule of thumb to give yourself a solid financial cushion is to have three to six months...

9.

Source: consumerfinance.gov

Title: how reduce your debt

Link:https://www.consumerfinance.gov/about-us/blog/how-reduce-your-debt/

Source snippet

Consumer Financial Protection BureauHow to reduce your debtJul 16, 2019 — There are two basic strategies that can help you reduce debt: t...

10.

Source: files.consumerfinance.gov

Title: Consumer Financial Protection Bureau Debt getting in your way?

Link:https://files.consumerfinance.gov/f/documents/bcfp_your-money-goals_debt_booklet_print.pdf

Source snippet

Get a handle on it.Con: If the interest and fees are high on your larger debts, you might pay more overall if you pay off the smaller one...

11.

Source: dictionary.cambridge.org

Link:https://dictionary.cambridge.org/dictionary/english/pay

Source snippet

something for something How much did you pay for the tickets? I pay my...Read more...

Additional References

12.

Source: researchgate.net

Link:https://www.researchgate.net/publication/260526717_Financial_Literacy_and_Emergency_Saving

Source snippet

(PDF) Financial Literacy and Emergency SavingThis paper investigates the correlations between subjectively and objectively assessed measu...

13.

Source: payments.service.gov.uk

Link:https://www.payments.service.gov.uk/

Source snippet

Pay has contracts with payment providers so you can take payments quickly and easily. It's used across central and local govern...

14.

Source: reuters.com

Link:https://www.reuters.com/markets/funds/how-build-an-emergency-fund-2025-12-16/

Source snippet

Despite its importance, more than 20% of Americans have no emergency savings, and only 46% are prepared to cover three months of expenses...

15.

Source: paypal.com

Link:https://www.paypal.com/uk/home

Source snippet

PayPal UK: PayPal Account | Mobile Wallet and MoreUse your PayPal account to spend, send, and manage your money. Or, create a merchant ac...

16.

Source: wearepay.uk

Link:https://www.wearepay.uk/what-we-do/overlay-services/request-to-pay/

17.

Source: chase.com

Link:https://www.chase.com/personal/banking/education/budgeting-saving/rainy-day-fund-vs-emergency-fund

18.

Source: alight.com

Link:https://www.alight.com/blog/how-emergency-fund-different-from-savings-account

Source snippet

It's a separate pool of money designated specifically to cover or offset expenses associated with an...Read more...

19.

Source: youtube.com

Link:https://www.youtube.com/watch?v=_xJh2uLRxaw

Source snippet

Learn How to Save Money and Pay Off Debt at the Same TimeBuilding your savings while paying off debt is just finding the balance of the r...

20.

Source: ithinkfi.org

Title: understanding emergency funds savings accounts in 2025

Link:https://www.ithinkfi.org/blog/blog-detail/ithink-blog/2025/10/01/understanding-emergency-funds—savings-accounts-in-2025

Source snippet

Understanding Emergency Funds & Savings Accounts in...1 Oct 2025 — Understand key differences between emergency funds and savings accoun...

21.

Source: reddit.com

Link:https://www.reddit.com/r/personalfinance/comments/1q6s5yy/need_advice_on_whether_i_should_save_for_an/

Source snippet

500 monthly just on ((interest)), or should I prioritize saving for...Read more...

Topic Tree